Century-old heritage brand Ghee Hiang has added a fresh chapter to its storied legacy. The iconic name, synonymous with traditional pastries and pure sesame oil since 1856, recently unveiled its Penang Series Cookies and a brand-new GH Cafe Corner at its Macalister Road outlet.

Local flavours are reimagined, to the delight of customers. The new cookie line features boldly inventive creations like Durian Cookies and Nasi Lemak with Anchovies Cookies. By blending familiar tastes with the brand’s time-honoured craftsmanship, this initiative is a playful yet respectful nod to Penang’s rich culinary identity.

The launch event, graced by guest of honour, YB Wong Hon Wai, Penang State Executive Councillor for Tourism and Creative Economy (PETACE), also marked the debut of the GH Cafe Corner—a cosy grab-and-go space where customers and visitors can enjoy freshly brewed coffee alongside warm, just-baked biscuits and pastries, enabling them to enjoy quality beverages while shopping for Ghee Hiang’s signature products. This simple but thoughtful addition turns a routine shopping trip into a sensory experience.

“We wanted to honour tradition while embracing new ideas,” said Executive Director, Dato’ Chng Huck Theng. “This is all about offering customers a more complete and enjoyable retail experience at Ghee Hiang,” he added.

For 170 years, Ghee Hiang has been a cherished part of Penang’s heritage. This year, the beloved brand marked its remarkable milestone with a triple celebration that honoured its rich history while embracing an exciting new future.

The festivities unfolded at its newly renovated Macalister Road outlet, which reopened its doors after its first major facelift since 2005. The space now beautifully balances old-world charm with contemporary elegance, offering a warm and inviting atmosphere for loyal customers and new visitors alike.

The momentous occasion was graced by Penang Chief Minister YAB Tuan Chow Kon Yeow, who joined in the unveiling of a special 170th-anniversary signboard and together with the guests, were treated to a vibrant lion dance and a spirited ribbon-cutting ceremony.

Inside, the revamped outlet showcases Ghee Hiang’s full range of beloved products—from time-honoured pastries and premium pure sesame oil to festive favourites that have graced dining tables for generations. Also taking centre stage was the launch of the 2026 Chinese New Year Gift Box, featuring refreshed packaging and signature flavours that capture the essence of Penang’s living heritage.

In a heartfelt speech, Dato’ Chng Huck Theng, Executive Director of Ghee Hiang, said, “As we celebrate 170 years, we are deeply grateful to generations of Penangites who have walked this journey with us. This milestone reflects our commitment to honour our heritage while embracing the future. We hope Ghee Hiang continues to be part of every family, young and old alike, bringing warmth, familiarity, and trust with every bite.”

The Penang Young Business Leaders 2026 edition is a timely and meaningful recognition of the dynamic individuals who are redefining what it means to lead in today’s business landscape. These young leaders span a wide spectrum – from technology and manufacturing to creative industries and social enterprises reflecting the diversity and agility of Penang’s economic ecosystem. The journey toward the Penang2030 vision requires bold, future-oriented leadership. Young business leaders play a critical role in this transformation. Through innovation, sustainable practices, and inclusive growth strategies, they are not just creating jobs – they are creating impact. Their success signals a broader readiness of our society to embrace change, adopt digitalisation, and lead with purpose.

Sunway Education Group CEO, Professor Elizabeth Lee is no stranger in the Malaysian higher education arena where she has been actively involved in the industry for the past 28 years. Her latest milestone in her achievements was when she was recently celebrated as the award winner in the Leadership Commitment category at the UN Women’s 2021 Malaysia Women’s Empowerment Principles (WEPs) Awards ceremony.

This award recognises corporate leaders who have been instrumental in setting strong corporate commitment including progressive policies, regulations or practices that aim to promote gender equality in the workplace, marketplace and community. This includes taking on specific roles and responsibilities to promote gender equality within the company and making public commitments or delivering gender-sensitive messages to the public.

Professor Lee believes that men and women bring different strengths to the workplace and the university is committed to advancing the United Nations Sustainable Development Goals (UN SDGs) especially in encouraging and promoting goals no. 4 – Quality Education, no. 5 – Gender Equality and no. 10 – Reduced Inequalities, through events, campaigns and on a daily basis.

Professor Lee continuously advocates gender equality among Sunway Education Group’s employees and students and frequently participates in various local and international forums and conferences related to education, gender equality and women empowerment.

She elaborated, “I am proud to say that at the Sunway Education Group, women make up more than 65 percent of the workforce, including top management roles. To ensure both our female and male employees’ welfare and wellbeing, we have various policies in place including Flexible Work Arrangements for Mothers, Anti-Sexual Harassment, as well as Diversity and Inclusion.

In accepting the award, Professor Lee credits the effort, commitment and dedication of her colleagues together with the firm support from the Board and Sunway Group Chairman, Tan Sri Jeffrey Cheah himself, who greatly advocates education, gender equality, women empowerment and the SDGs.

by Calvin Goon, Head of Wealth Management, Affin Bank Berhad

Achieving financial goals may sound big to a lot of people and often takes a little more effort than just luck. However, is it unachievable at all?

Just like any of the large task we have, it will sound less difficult if we break them it into smaller sub-tasks. The key here is taking “Baby Steps”. Try to improve your financial wellness by challenging yourself into taking some of these baby steps below:

Again, it might seem difficult to start despite breaking your large financial goals down into “Baby Steps” but you will be astounded by how your financial position will improve once you start to follow through all these steps gradually.

At Affin Invikta, we can help you start your Baby Steps by offering customized financial solutions tailored to your needs. Want to know more? Reach out to us at www.affininvikta.com and we will assign a dedicated Relationship Manager to guide you through.

Scan here to know more about Affin Invikta

Success is not overnight. It all starts with ‘BABY STEPS’

by Kenny Teoh, Managing Director, Hectarworld Group

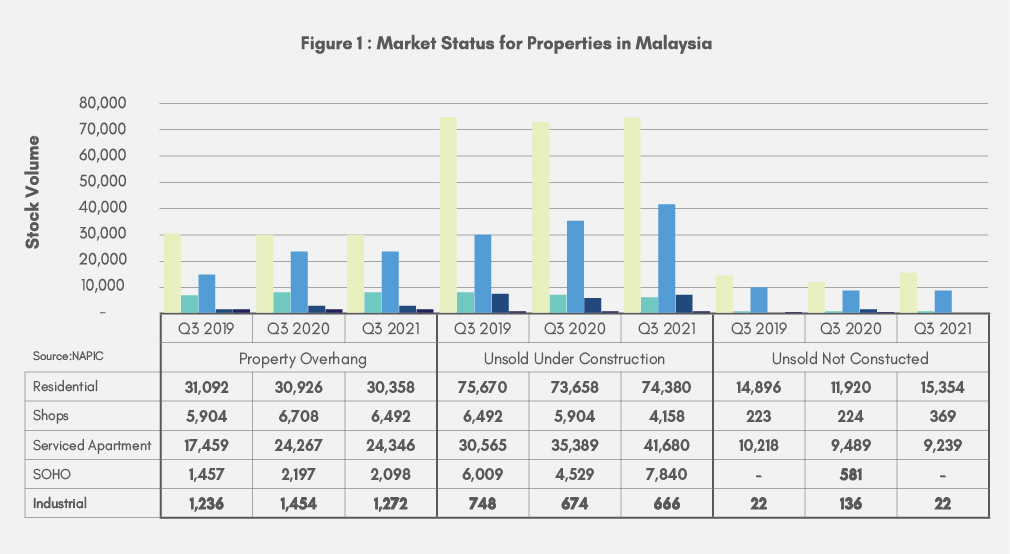

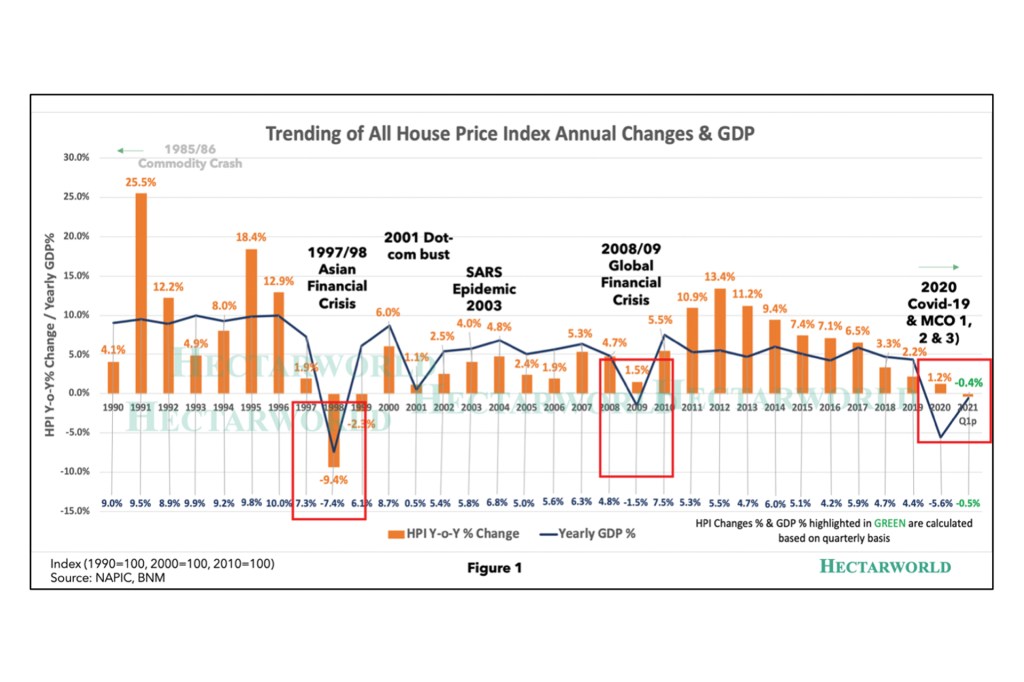

The supply overhang remains a concern to most Malaysians in general as according to the National Property Information Centre (“NAPIC”) data in Figure 1 below, a total of 30,358units of completed houses were reported unsold in the third quarter (Q3) of 2021, and by state with reference to Figure 2, 3, 4 and 5 respectively, Johor has the highest number of unsold units(21 per cent share) in Malaysia, followed by Penang (15 per cent), Kuala Lumpur (13 per cent) and Selangor (11 per cent).

According to the definition by the NAPIC, overhang is defined as residential units which have received Certificate of Completion and Compliance (CCC) but remained unsold for more than nine months after launch.

A property overhang reflects an area of the market where the supply of available properties is higher than demand. Among the factors that contributed to the property overhang were changing economic conditions, supplies that did not match demands in localities, prices and household income, and unattractive locations of housing projects.

New launches will contribute to the overhang situation if developers do not accurately assess or predict local market conditions, then they may ultimately end up oversupplying the market.

The property market’s performance for the third quarter of 2021 (Q3 2021) is expected to remain stagnant due to the impact from enforcement of Movement Control Order (MCO 3.0),. Pent-up demand is expected by early Q1 2022 after the government lifted the MCO 3.0.

Nevertheless, Malaysia’s property market remains relatively resilient due to the strong financial position of property developers and banks’ continued lending.

This property overhang situation is expected to remain stable amidst efforts by developers to clear unsold completed properties at a reasonable price and measures taken by Malaysian Government like the Home Ownership Campaign (HOC) and low interest rate regime to encourage more home ownership especially for first-time home buyers.

Data by the NAPIC revealed a 1.83 per cent decrease in the number of unsold residential units in the third quarter of 2021 compared with the third quarter of 2020 (a total 30,926 unsold completed houses).

This slight drop in unsold housing properties was attributed to numerous promotional efforts by developers including reducing prices or offering discounts to house buyers.

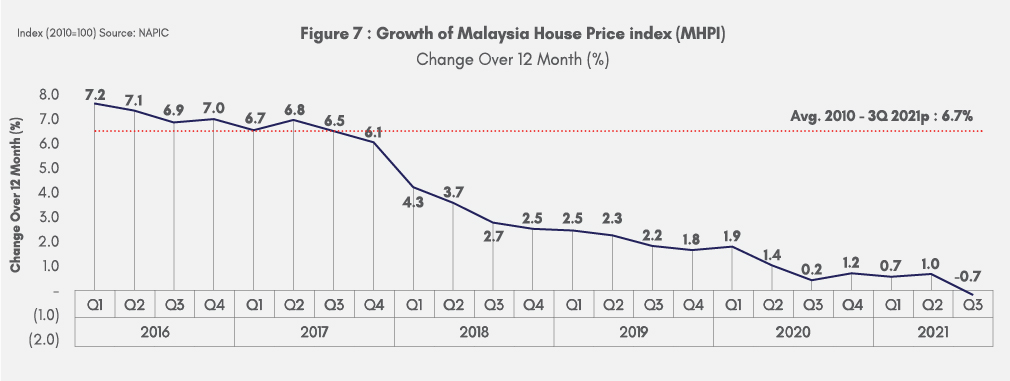

“This was shown by the reduction in the House Price Index in the third quarter of 2021 (preliminary) recorded at 198.6 index point compared with the third quarter of 2020 at 199.9, which is a 0.7 per cent drop (as shown in the Figure 7 below)

The current low Overnight Policy Rate (OPR) of 1.75 per cent since July 7, 2020, and the HOC which offered duty stamp exemption and a 10 per cent discount on houses priced between RM300,000 and RM2.5 million by developers registered with the Real Estate and Housing Developers’ Association Malaysia (REHDA) till year-end of 2021 have helped shore up residential property sales, easing the overhang in the segment in the third quarter.

Most prospective buyers are owner-occupiers who capitalise on the low interest rate and incentives offered under HOC or by the developers. The young population and first-time house buyers are the main factors that drive the demand for properties.

What is next for the property sector and house buyer like you and I?

It’s a buyer’s market now!

During the pre-pandemic period, the sheer number of newly completed and handover units in the market had shifted the bargaining power in the property market to house buyers.

In the case of an oversupply of property market, a house buyer might even be able to find a great deal with many perks from developers and banks. House buyers can try and negotiate for reduced prices or sweeteners like freebies or discounts are more likely to happen in a buyers’ market.

Malaysian economy is expected to gain momentum after the government lifted the MCO since Q3 2021 and is preparing to enter epidemic phase with possible opening of borders in 2022. Based on recent preliminary claim made by Bank Negara, the overall economy will expand between 5.5% and 6.5% in 2022. Firmer property market from H2 2022 onwards will be expected driven by the economic recovery as income may rise and turn into greater purchasing power. There could also be spill over effects to property market from strong commodity prices and stock market gains.

Some people may take offence at the title of this article, claiming it to be rather unsympathetic towards many people who are not doing so well due to the surrounding circumstances. I would urge you to think otherwise. In fact, I am writing this piece for everyone who may not think one can be a winner, with the hope of turning you into a winner!

First of all, you’d agree with me that there are winners, especially those in the so called ‘right’ industries like e-commerce, healthcare, selected technologies, last-mile deliveries and a few others. If industry is the only defining factor, why are there businesses within the above-mentioned industries which are not doing just as well? On the other hand, there are also businesses in other industries that are out-performing the rest, increasing their market values in 2020. Check out Tesla, China Tourism Group, Fortescue Metals Group and many others. Nike even recorded their 50-year historical best in their most recent fiscal quarter.

If you are not convinced that you can be in the same league as the businesses above, let me give you more good news. About a year ago, we would read reports that the world economies will be facing contractions, with the exceptions of China. Fast forward to today, according to the Global Economic Prospects published by the World Bank Group in June 2021, economies are forecasted to enjoy positive growths across the globe. The statistics seem to suggest that we are beginning to kickstart an upward trend. The question now is are we ready to ride the wave of growth?

Source data: The World Bank (June 2021)

So, snap out of it! Please don’t use the Pandemic as the excuse! You’ve got to start by believing that you can be a winner! We cannot just hope that everything will just automatically return to normal one day but we do need to believe that the light at the end of the tunnel is in sight. We’ve got to commence actions to adjust our trajectory towards the winning direction. Some might be asking their astrology masters when is the right time? No timing is better that NOW!

So, what can we do? My friends, that’s another story…

In early 2020, the Covid-19 pandemic came as a global shock that tore many peoples’ lives asunder and left all of us worried about our finances. During these uncertain times, many would perceive cash as king, holding on to as much of it as possible to play it safe.

But is this really the best strategy?

In fact, one key indicator of the growing economic uncertainty this year is the fact that Bank Negara Malaysia has recently reduced the Overnight Policy Rate (OPR) by 125 basis points to a record low, a level that was last seen only during the 2008 global financial crisis. This move is one of several aggressive monetary measures, aimed at injecting liquidity back into the economy and thus putting it on the road to recovery. As a result, fixed deposit rates have been lowered at all Malaysian banks.

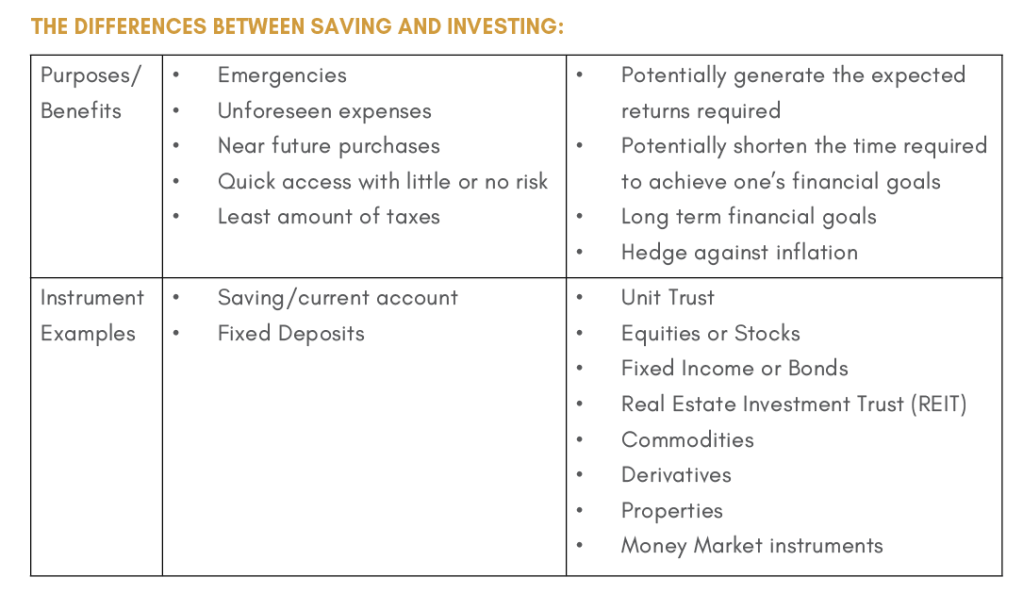

These developments, together with the undetermined duration of this prolonged pandemic and the adverse effects of a low interest rate environment, may make a person doubt their wealth strategy, which is why having an actual plan for your money has become more crucial than ever. One way to solidify your wealth involves saving and investing interchangeably, but with key differences; it is important to note that these two instruments serve different purposes.

The Differences Between Saving and Investing:

In a truly solid Wealth Management plan, savings and investments should not be a question of one or the other, but rather a blend to complement each other. If you are a big fan of fixed deposits, you may need to consider diversifying your funds into investments as well in order to let the money work harder for you. Ultimately, the best strategy involves understanding the characteristics, benefits, and risks of saving and investing. Subsequently, you should choose the best ratio that combines both to suit your risk tolerance.

Remember, don’t put everything into one basket!

Oftentimes, the “killer” of your wealth management strategy is not how you invest, but the misconception and myths most people have heard about investments. As such, it is always important for a person to fully understand the risk-reward trade offs before making any commitment to an investment. As risk appetite may vary for different people (clients), it is essential to categorise their individual risk profile into categories: Conservative, Balanced, Growth, and Aggressive to effectively plan a unique investment portfolio. For example, utilising equities as an investment to generate higher potential returns works for a client with an Aggressive risk profile, while utilising bond investments is more suited to a client with a Conservative risk profile. Without exception, recognising the type of risk a client has is of utmost importance for investment portfolio planning, as a client with a lower risk tolerance may not be able to stomach a strategy with higher risk.

If you’re ready to start or improve your wealth management strategy, consider AFFIN INVIKTATM; we are experts in recognising a client’s risk profile and tapping on available investment options to sculpt a portfolio that is best suited to your risk appetite and personal financial aims.

With us, it is always about you, your money and achieving your financial goals.

“Poor people see a dollar as a dollar to trade for something they want right now. Rich people see every dollar as a ‘seed’ that can be planted to earn a hundred more dollars… then replanted to earn thousand more dollars.” (T. Harv Eker, Secrets of the Millionaire Mind)

Prior to the Covid-19 pandemic in 2020, issues such as property price affordability and oversupply are already affecting overall Malaysian property market. The Movement Control Order (MCO) since March 2020 and closed borders due to Covid-19 have inevitably caused uncertain economic outlook, weak business and consumer confidence. As a result, prospective buyers and investors are currently adopting a “wait and see” attitude. All these factors have further exaggerated the overall sluggish Property Market since 2020.

However, the Covid-19 pandemic is expected to be under control by this year-end, supported by our National Vaccination Programme that has been going full force since June 2021. This roll-out of the vaccination programme will surely help speed things up and hopefully allow the country and its people to get back to their new normal lives and restart most business activities that were negatively affected since the beginning of this pandemic. At the time of writing this article, our new Health Minister, Khairy Jamaluddin claimed that 80% of the Malaysian adult population are targeted to be fully vaccinated by end of October 2021 and the country can expect to move from the Covid-19 pandemic into an endemic by then; a phase where we start living with the virus.

The overall property market is expected to rebound and experience pent-up demand when our lives and business activities are progressively restored by year end. Property market growth depends very much on the country economic growth rate. The historical trend is a testament to this relationship.

As shown in Figure 1 above, the Asian financial crisis struck our country in 1997 and the market did badly in 1998 at – 9.4% GDP Growth, but recovered almost immediately in 1999 at 6% GDP Growth. Similarly, the Subprime mortgage crisis in 2008 saw the market plunged in 2009 and again positively recovered by 2010 onward. During early 2020, Covid-19 pandemic hit our country and the GDP Growth started to decline at about -0.4% to -0.5% at Q1 2021 and expected to stay sluggish throughout 2021 due to the implementation of Full Movement Control Order (FMCO). Positive recovery is expected in 2022 when new normal is restored and the health crisis is brought under control through herd immunity.

Regardless, current property market is quite conducive for first time home buyers and property investors due to the low-interest rate regime and “hit rock bottom” property price (as shown in the Figure 1 above) even in some matured locations. In addition, the government’s allocations in the Budget 2021 to revive and ensure the continuity of mega infrastructure projects and the extension of Home Ownership Campaign (HOC 2020-2021) till Dec 2021 would be much needed boosters to the overall property market.

We will be at the end of the tunnel soon, and we expect the economy to reopen when the country achieves its targetted herd immunity by end of October 2021. Property market will start to rebound by year end and begin its positive recovery in 2022 onwards.

by Aida Lim Abdullah, CEO of Penang Halal International Sdn Bhd, A State Govt Owned Entity

(CGMA, CIMA, CA, CFP, CSI, BA (Hons) Accounting & Finance (major in law))

Within approximately 45 years, the Global Modern Islamic finance has grown to an asset size of about USD2.5 trillion as reported in 2018, represented by almost 1,500 institutions worldwide (Islamic Finance Development Report 2019), whereas, “The Economic Outlook 2021” report published by the Ministry of Finance (MoF), Malaysia, shows that the Islamic banking industry in Malaysia has a total asset valued at RM1.03 billion and the total outstanding Islamic financing is about RM787.8 billion.

Islamic Financing is not only for the Muslims. It is a fast-moving industry, alongside the development of Syariah and Halal business activities. The Islamic financial system operates with the principles of Shariah law where elements such as usury (riba), ambiguity (gharar) and speculation (maisir) are prohibited. In this regard, Bank Negara Malaysia (BNM) and the Securities Commission (SC) have prescribed approved Shariah principles that apply to banking, insurance and capital market products in Malaysia; for example:- mudharabah (profit-sharing), murabahah (cost-plus sale) and tawarruq (tripartite sale).

HOW IS THE ISLAMIC FINANCE AND BUSINESSES IMPACTED BY THE COVID-19’S PANDEMIC?

The fallout from the Covid-19 pandemic and its effects on the world’s economy surpassed that of the global financial crisis in 2008. The unprecedented Covid-19 crisis created severe uncertainty and struck a dire blow on global economy and international trade. The negative economic and human impact with far-reaching implications on consumer, corporate, and global trade finance dynamics swept around the globe with lightning speed.

Nevertheless, based on the MoF report, it is expected that Malaysia’s Islamic finance industry is likely to expand further with the continuous promotion of Shariah-compliant products. As the financial industry and business environment evolves, there are more Shariah-compliant products introduced and are available in the local market for Muslim and non-Muslim investors and businesses.

The Covid-19 pandemic has also created awareness on the use of financial technology offerings in the area of Islamic finance such as Shariah-compliant digital assets, crowdfunding and peer-to-peer financing platforms with a suite of e-Commerce set-ups that offers Halal goods, like those initiated by Penang Halal International with its partners namely, Penang E-Mall@Shopee, Foodpanda, Food4U programme and Penang E-Bazaar@PGMall.

Globally, we are seeing some countries downsizing or even shutting down certain industries and sectors; the economic hardships observed have amplified and spilled over to all. Those who can work from home mostly have stable incomes, but non-permanent or daily workers are at risk of losing their earnings, particularly in the most affected industries such as property, construction, tourism and service industry.

CONCLUSION:

One of the important wake-up calls in this pandemic is that many now realise the importance of embracing ethical and hygienic lifestyles, especially in the food chain process from manufacturing, processing to consumption. As such, it would seem that the Islamic Finance will continue to develop and grow upwards alongside with Syariah, Halalan Toyyiban lifestyle, be it for religion or just an individual choice for ethical and hygienic lifestyle. There appears to be a bright future for Islamic Finance and Businesses moving forward.