by Calvin Goon

Head of Wealth Management, Affin Bank Berhad

Which Strategy Works Best for You?

In early 2020, the Covid-19 pandemic came as a global shock that tore many peoples’ lives asunder and left all of us worried about our finances. During these uncertain times, many would perceive cash as king, holding on to as much of it as possible to play it safe.

But is this really the best strategy?

In fact, one key indicator of the growing economic uncertainty this year is the fact that Bank Negara Malaysia has recently reduced the Overnight Policy Rate (OPR) by 125 basis points to a record low, a level that was last seen only during the 2008 global financial crisis. This move is one of several aggressive monetary measures, aimed at injecting liquidity back into the economy and thus putting it on the road to recovery. As a result, fixed deposit rates have been lowered at all Malaysian banks.

These developments, together with the undetermined duration of this prolonged pandemic and the adverse effects of a low interest rate environment, may make a person doubt their wealth strategy, which is why having an actual plan for your money has become more crucial than ever. One way to solidify your wealth involves saving and investing interchangeably, but with key differences; it is important to note that these two instruments serve different purposes.

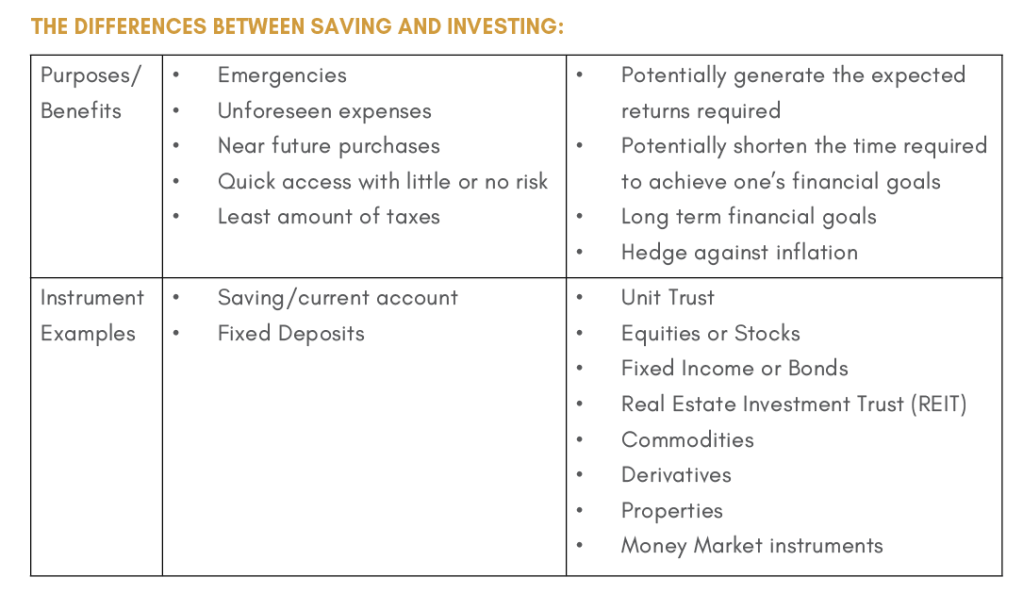

The Differences Between Saving and Investing:

In a truly solid Wealth Management plan, savings and investments should not be a question of one or the other, but rather a blend to complement each other. If you are a big fan of fixed deposits, you may need to consider diversifying your funds into investments as well in order to let the money work harder for you. Ultimately, the best strategy involves understanding the characteristics, benefits, and risks of saving and investing. Subsequently, you should choose the best ratio that combines both to suit your risk tolerance.

Remember, don’t put everything into one basket!

Oftentimes, the “killer” of your wealth management strategy is not how you invest, but the misconception and myths most people have heard about investments. As such, it is always important for a person to fully understand the risk-reward trade offs before making any commitment to an investment. As risk appetite may vary for different people (clients), it is essential to categorise their individual risk profile into categories: Conservative, Balanced, Growth, and Aggressive to effectively plan a unique investment portfolio. For example, utilising equities as an investment to generate higher potential returns works for a client with an Aggressive risk profile, while utilising bond investments is more suited to a client with a Conservative risk profile. Without exception, recognising the type of risk a client has is of utmost importance for investment portfolio planning, as a client with a lower risk tolerance may not be able to stomach a strategy with higher risk.

If you’re ready to start or improve your wealth management strategy, consider AFFIN INVIKTATM; we are experts in recognising a client’s risk profile and tapping on available investment options to sculpt a portfolio that is best suited to your risk appetite and personal financial aims.

With us, it is always about you, your money and achieving your financial goals.

“Poor people see a dollar as a dollar to trade for something they want right now. Rich people see every dollar as a ‘seed’ that can be planted to earn a hundred more dollars… then replanted to earn thousand more dollars.” (T. Harv Eker, Secrets of the Millionaire Mind)